Here Comes Another Cut, But Will the Markets Celebrate?!?!

What to Expect Today

The Federal Open Market Committee (FOMC) is going to cut interest rates by another 1/4% at 2:00pm on Wednesday. The market is expecting it and the cut has already been priced in. Any other action would be a shocker. With stocks so close to all-time highs, this is again reminiscent of 1995 when the Fed came from an overly restrictive monetary policy in 1994 to realizing they screwed up and quickly played catch up. Stocks had long understood and priced this in with 1995 being one of the all-time great investing years in modern history.

Right after the Fed announces their decision, all eyes will be on the statement for clues of future interest rate cuts or signs that the Fed may be close to being done. The stock market will definitely not like a rate cut with a hawkish statement, meaning comments from the Fed that they are not looking for more cuts ahead. I find it hard to believe that Jay Powell & Company will cut rates and then prepare the markets for more rate cuts this year.

Model for the Day

As with every Fed statement day, 90% of the time stocks stay in a plus or minus .50% range until 2pm before the fireworks take place. I fully expect that to be the case today. Besides that, there is also a strong long-term trend for stocks to close the day higher, although that is not as strong as it used to be. Additionally, with stocks near all-time highs and significant upside progress over the past month, the bulls have even less dry powder than normal, not to mention how poorly stocks have done under Jay Powell on Fed day. 6 weeks ago, I offered that “any short-term rally may be sold”. From 2:00pm on July 31 until August 5, stocks fell in a straight line after Powell et al indicated that the rate decrease was a “mid-cycle cut” and not the beginning of a new accommodative cycle.

Jay Powell’s Arrogance & Ignorance

As I already mentioned, everyone knows what the Fed is going to do at 2:00 pm today. That’s not in debate. And right now, the market is pricing in at least another rate cut. Long time readers know that I have been very critical of the Fed, more with Yellen and Powell than Bernanke although Big Ben did make perhaps the single greatest imbecilic comment in 2007 when he said the sub prime mortgage crisis was “contained” and there would be “no contagion”. It would be impossible to have been any more wrong than that and on an epic scale.

Anyway, I think the Jay Powell led Fed is among the worst groups since 1988 when I entered the business. Greenspan may have been the worst Fed chair since Arthur Burns in the 1970s but Powell is certainly working on his legacy and it’s not an enviable one.

For 6 years I have pounded the table that raising interest rates AND selling assets which is now being referred to as quantitative tightening is the mistake of all mistakes. Selling assets is akin to also hiking rates as it reduces liquidity and tightens financial conditions. Janet Yellen should have chosen one or the other. Pick your poison. Instead, she forged ahead with both.

Jay Powell continued on that path except he, in a grand stroke of additional arrogance, decided that rates should go up at a quicker pace. Arrogance and ignorance are among the two worst character traits and I think Powell has them both. We all saw what happened last December when the Fed added that one additional rate hike and did not temper the asset sales. The global financial markets collapsed like hadn’t been seen since the Great Depression.

The Fed – Savior of the Financial Markets

Now, you can argue that it’s not the Fed’s job to appease the financial markets and you would technically be correct. The Fed has a dual mandate from Congress. Price stability (inflation) and maximum employment. However, the Fed, for the most part, usually follows what the markets want and have priced in. I say “usually” because there have been a few times when the Fed has gone off book.

Remember, the Fed doesn’t want to upset the financial markets. These markets are absolutely vital the U.S. and global economies. And despite what you may hear from Lizzie Warren and Bernie Sanders, a healthy and vibrant Wall Street community is an absolute necessity to a growing economy, even though that same group is prone to bouts of greed and bad behavior which can have a periodic and significant detrimental impact on the economy (see chapter on how the financial crisis began in 2007 and 1929).

When politicians from both sides talk about how Wall Street “wrecked” the economy, they always forget how many direct and indirect jobs were created from Wall Street’s work. The problem is that we (the U.S.) always seems to reward bad behavior and don’t punish it. And so many politicians continue to pat themselves on the back for the Dodd-Frank piece of legislation which did good by increasing capital standards but failed miserably by declaring victory that the days of Wall Street bailouts were over. Not a chance.

When push comes to shove, the political will is never there to let a Morgan Stanley or a Goldman potentially take down the economy. In real time in 2008, my thesis was that AIG should not have been saved which would have sent Goldman down with it. I thought letting more institutions be punished would have caused more short-term pain, but the free market would picked up the slack and the economy would have seen a much, much better recovery than it did. A topic for a different day.

Dual Mandate

As I already mentioned above, the fed has a dual mandate from Congress. Regardless of what President Trump believes or wants, the Fed’s instructions are from Congress. When we look at the Fed’s dual mandate, Congress essentially directs the Fed to keep inflation manageable and seek to have the country fully employed.

Right now, unemployment is at or near record lows with minority unemployment also at or near the lowest levels since records began. That is maximum employment, a point where the Fed would normally worry about a labor shortage and a spike in wages. While wages are finally rising, we are not seeing a squeeze and nothing like McDonalds paying signing bonuses like we saw years ago. With half of the Fed’s mandate pointing towards a rate hike, it’s makes me wonder.

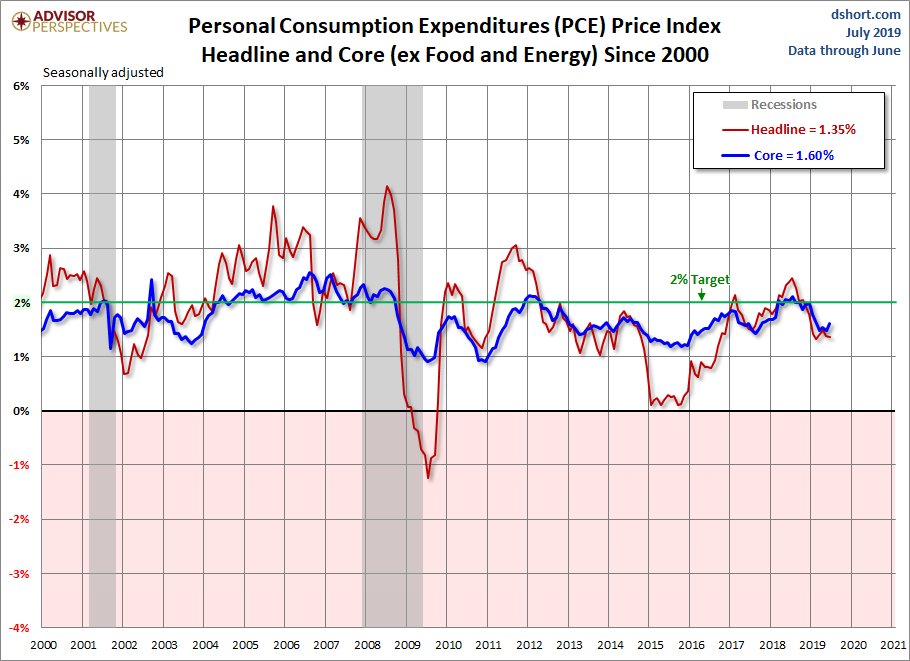

Looking at price stability (inflation), we see the same trend that has been in place for more than a decade; inflation cannot seem to get going. While many people are familiar with the Consumer Price Index, the chart below is a much better gauge and you can Google if you want more info about it. The blue line excludes food and energy and this CENTURY you can’t find a single year of 3%. The very random Fed target of 2% has barely been met since the financial crisis.

So, the second half of the dual mandate is certainly amenable to a rate cut although the most recent data was just a tad “hotter” than the market was expecting. You have the dual mandate at odds. In my world, that would mean a neutral stance by the Fed. Leave rates unchanged and stop selling assets, which they did announce at the July meeting.

Jay Powell & Company at Odds

Jay Powell and the majority of the voting members of the Fed want to cut interest rates by 1/4%. There is a minority faction that wants to leave rates alone. Powell has spoken about an “insurance” rate cut which in my mind means a single cut. Today, we are look at cut number two. He discussed weakening economies in Europe and Asia that eventually could impact the U.S. I just want to know where in the dual mandate it says that the Fed should worry about China and Europe. The rest of the world is now loosening financial conditions so now Powell wants to follow them.

ECB chief Mario Draghi is on his way out of Dodge, leaving Europe in worse shape than when he began 8 years ago. With more than $15 trillion in negatively yielding bonds and a whole new round of bond buying starting, Europe is that fly in search of the windshield. That story ain’t gonna end well. However, the powers that be refuse to accept their fate. The Euro experiment is a failure, plain and simple. It should be dismantled, but I digress.

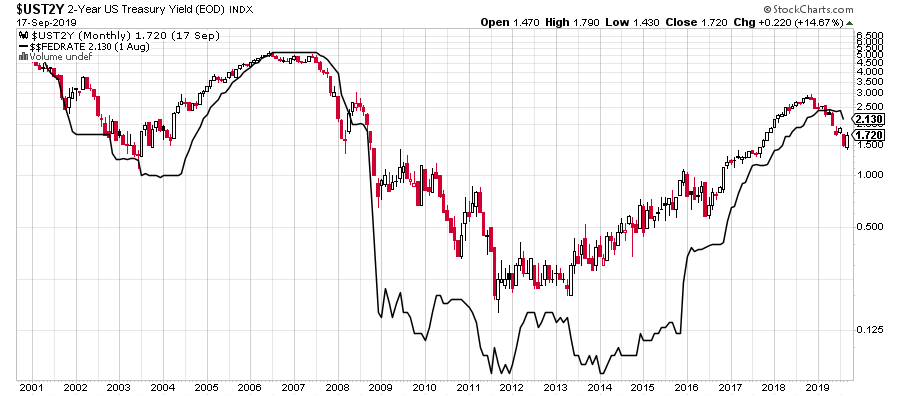

The markets are expecting 1/4% cut. One of the many great charts and work that Tom McClellan does has to do with forecasting a rate move based on the two-year Treasury Note. Below is a chart of that instrument overlayed with the Federal Funds Rate which is the actual interest rate the Fed controls. Tom argues that all the Fed needs to do is follow the two-year Note instead of meeting and debating all the time. His analysis certainly has merit.

When the solid black line is below the colored line, the Fed is allowing easy financial conditions. The reverse is true when it’s above the colored line. Right now, the two-year Note (the market) is telling the Fed to cut rates although a little less than it did 6 weeks before the Fed’s last meeting. While I believe it’s premature, the market does not.

What I Would Do

While I could go on and on and on as I sometimes tend to do, I am going to wrap this up by saying that Powell is going to hide behind tariffs and China as the reason to cut rates today. Although I absolutely do not think he will intend to poke the President, I do think that labeling tariffs as the potential economic weakness culprit will certainly tweak Donald Trump.

My own economic forecast remains unchanged since I first offered it in late 2017. I think the U.S. will experience a very mild recession beginning before the 2020 election. Although there are so many doom and gloomers who forecast something much more ominous, it’s almost impossible with the banks in such great shape, literally sitting on more than two trillion dollars in cash. And if you want to know what I would do instead of cutting rates, I would stop paying the banks to keep their excess reserves at the Fed. This would force them put some money to work in the economy.